Curriculum

MODULE 2 - Defining your Social Business

Unit 1 – Business Model Canvas for social enterprises

0/8Unit 2 - Finance & fundraising

0/13-

Unit 2 - Details

Trial

Trial -

Case Study

Trial

-

Lesson - introduction

Trial

-

Lesson - Expenses: Types of Costs

Trial

-

Lesson - Break-even Analysis

Trial

-

Lesson - Profit and Loss Account

Trial

-

Lesson - Cashflow Forecast

Trial

-

Lesson - Finance and Stakeholders

Trial

-

Tips & Tricks

Trial

-

Important concepts/definitions

Trial

-

Self-reflective questions

Trial

-

You may also be interested in this/ Additional useful resources

Trial

-

References

Trial

Unit 3 - Legislation

0/1Unit 4 – Marketing for social enterprises in the field of gastronomy

0/8Lesson – Expenses: Types of Costs

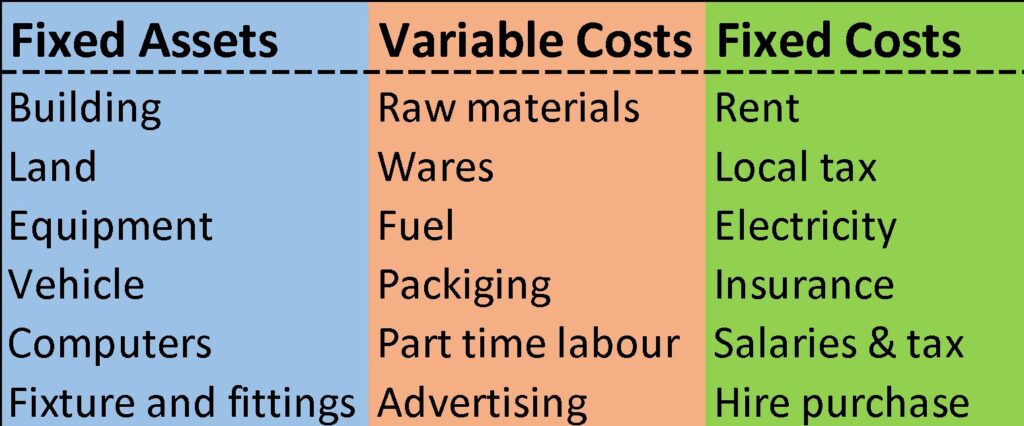

The following will help when structuring the financial information for the social enterprise plan and will help you to identify appropriate types of finance for different types of costs. There are three types of costs, these are:

Fixed Assets ― one off purchases that retain financial value, for more than one year.

Variable Costs ― the costs of directly producing the product/service.

Fixed Costs ― on-going costs regardless of the sales or other activities.

The easiest type to obtain is a fixed asset as the item purchased retains much of its value and can therefore always be sold to repay the raised finance. Fixed Asset costs are considered low risk and easier to obtain. On the other hand, they are harder to liquidate, meaning that turning them into money is not easy ― e.g. how often do you buy a house or a piece of land. Fixed Assets are exchanged in sluggish processes, therefore usually have slow markets.

Finance to cover variable costs is harder to raise because these costs only retain part of the purchase value or have little return on investment. But in the event of something going wrong items like raw material can be sold easily to repay raised finance. Variable costs can be considered medium risk.

Fixed costs, however, are those you have to pay regardless of whether or not you sell anything. They have very little resale value ― e.g. it could be tough to resale your rental right, after you paid for it in advance ― these are very difficult to raise finance against as they have no inherent value once spent.

How to count for costs: Identify Unit Costs

Early on in your financial planning it is useful to try to develop a unit value against which you can start to calculate the cost of producing the product/service and the number of units you think can be sold in one year.

A unit is your product/service broken down into something you sell ― e.g. restaurants sell lunch, one main course and either a starter or a dessert. In terms of services, you should use a unit of time either an hour, day or week which will have a cost. Sometimes units may consist of both a physical item plus a time element for servicing or delivering the physical item. Whatever your commercial idea is see if you can break it down into units of some sort however rough and ready they are at this stage.

The unit cost will be made up of:

- Variable costs: The purchases of material, packaging, direct labour and any costs that vary in relation to the volume (the number of units) produced or provided. This can also include delivery if this is part of the direct selling.

- Fixed costs: The costs for such things as salaries, rent, utilities, etc. are included in the unit cost by apportioning a percentage of the cost to each unit produced in one year.

- Fixed Assets: These are paid for over a fixed time period as depreciation[1] in the Profit and Loss Account ― more on that later ― and again you will need to apportion a percentage of the total depreciation to the cost of each unit.

To work out a unit cost determine the number of units you can produce/supply in a year and then divide by the total cost for running the enterprise ― this must include depreciation costs for fixed assets, direct variable costs and fixed costs for the year. This could be a general estimation, it doesn’t have to be exact. Pay special attention to the time period you are working with, unit costs are usually calculated on an annual basis as earlier suggested:

More elaborately:

*Remember units can also be defined by time

At this point you can also start to think of the total profit you are likely to make by calculating profit for each unit sold multiplied by the volume sold ― again pay attention to the time period.

![]()

BUT in some circumstances the higher the volume the lower the unit cost as fixed costs remain the same until you reach a point where the fixed costs have to increase to meet the needs of a higher volume production. Also, in case of a social enterprise it’s advisable to count for other ways of income and/or to lower your production costs ― tenders, tax allowances, involvement of volunteers etc. ― however, it’s always better not to be dependent on those to make a profit.

[1] Help to calculate depreciation: Fresh Books