Curriculum

MODULE 2 - Defining your Social Business

Unit 1 – Business Model Canvas for social enterprises

0/8Unit 2 - Finance & fundraising

0/13-

Unit 2 - Details

Trial

Trial -

Case Study

Trial

-

Lesson - introduction

Trial

-

Lesson - Expenses: Types of Costs

Trial

-

Lesson - Break-even Analysis

Trial

-

Lesson - Profit and Loss Account

Trial

-

Lesson - Cashflow Forecast

Trial

-

Lesson - Finance and Stakeholders

Trial

-

Tips & Tricks

Trial

-

Important concepts/definitions

Trial

-

Self-reflective questions

Trial

-

You may also be interested in this/ Additional useful resources

Trial

-

References

Trial

Unit 3 - Legislation

0/1Unit 4 – Marketing for social enterprises in the field of gastronomy

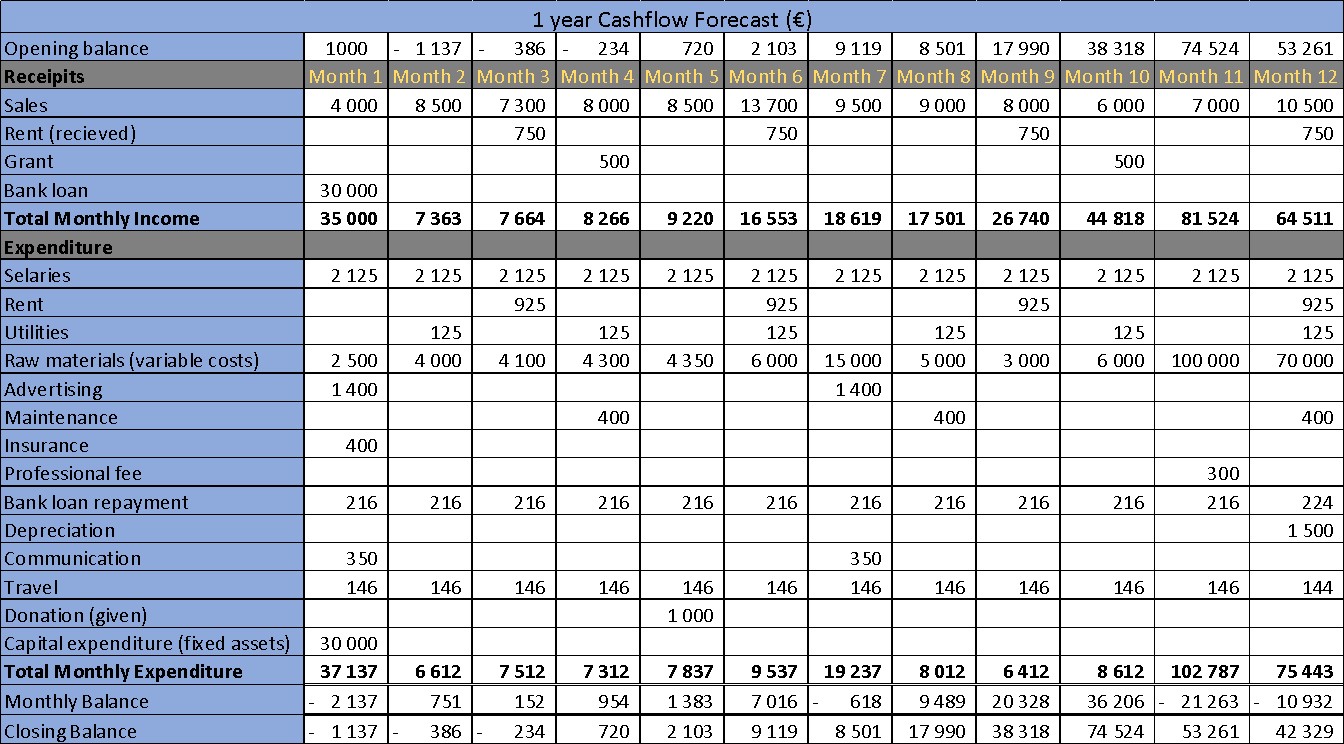

0/8Lesson – Cashflow Forecast

Although it is called a Cashflow Forecast (CF) it really relates to all monies in and out of the enterprise’s bank account. The CF shows the same information but in a different way, it shows how the ‘cash’ flows instead of if you have made a profit or loss. The profit and loss account shows income, expenditure and profit or loss, while the CF shows the actual state of the enterprise’s financial position at any particular time. The very critical difference is that it is possible to show a profit in the PLA wasn’t showing a minus in the CF. Both will be true reflections of your finance.

Many small and new enterprises that will make a profit in the longer run go bankrupt in the short term because they run out of cash to pay the bills. Management must understand this. You must use the CF to manage the enterprise on a daily/weekly basis. For the Social Enterprise Plan the CF should be prepared for three years; this is normal practice.

You use the same headings and figures in both the PLA and the CF however, in the CF you spread the figures out month by month. Each entry should reflect the actual receipt or expenditure of money for the particular month. The more accurate you are the more control you will have managing your finance.

Where there is an increase or decrease in anticipated sales or costs you should reflect that in the monthly amounts. It is important to reflect seasonal and weather fluctuations in the monthly figures, for example, some enterprises sell more at different times of year, also there are higher or lower heating/cooling costs at different times of year, and these should be reflected in the Forecast. Also, payments for expenditure and receipts from customers should be planned for when the financial transactions actually take place, so if you pay or receive some bills in advance or in arrears this should be reflected in the CF.

It is advisable to ‘play around’ with the figures to see how to get the best for you. For example if you are carrying a high negative cash flow then see if you can pay your bills later or bring forward payments to you from customers, but if you have to borrow cash to cover the negative cash flow then make sure you secure enough to cover the highest monthly negative balance.

Remember CF and PLA are different:

- The CF indicates the amount of money that has been spent and the amount of money that has been received at any given point. The PLA also includes monies that are owed to the enterprise and monies that are owed by the enterprise to others.

- The balance between what is owed and what is owing can be very different from the actual cash that is available at any particular time.

- CF help you identify short term flows in your income

- PLA will give you an insight of medium / long-term resources required to help you develop your activities.